JazzIRT

Company Snapshot

Medical Properties Trust (NYSE:MPW) is a healthcare REIT that has been around for close to two decades. During that time, it has managed to gain access to 46,000 licensed hospital beds across 17 states, making it the second largest owner in the US. Besides the US, it also has operations in Europe, Australia, and South America. In addition to its core expertise of acquiring, developing, and leasing healthcare facilities under long-term contracts, it also provides mortgage loans and other types of loans (via its subsidiaries) to healthcare operators. MPW also looks to secure equity ownership with some of its tenants.

What’s To Like?

MPW has quite a few interesting qualities that could enable it to serve as a fine portfolio stock over time.

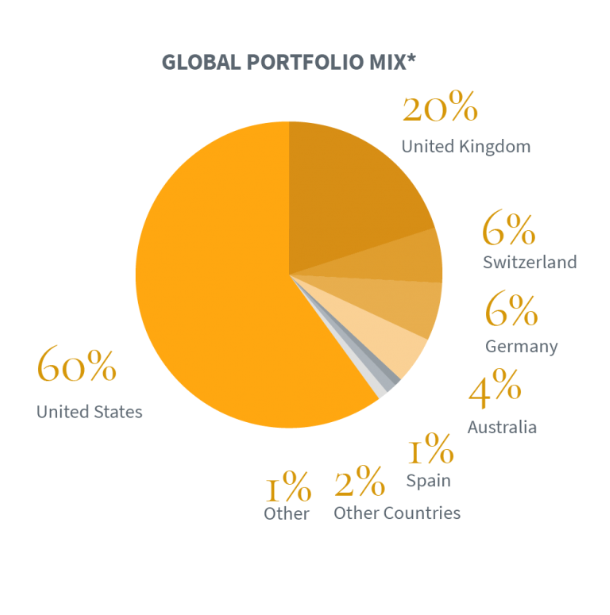

Firstly, it primarily operates in a very lucrative market- the US; 60% of its business comes from this market which is proving to be a very opportunistic terrain for those who are involved. The country tops the world for total healthcare expenditure ($4.1 trillion); this equates to $12,530 per person and is poised to grow at over 5% CAGR and reach $6.2 trillion in six years. As a percentage of GDP, the US already spends more than anyone else at 19%. Within the US, MPW is also not dependent on only certain pockets as no single state accounts for more than a 10% share.

MPW Website

Then there’s a lot of brouhaha about inflationary pressures across the economy, but MPW is one of those entities that look well-positioned to cope with these conditions. Firstly, do note that Medicare reimbursements that hospitals receive are typically higher than inflation. Besides 99% of MPW’s lease agreements have, either annual rent escalation costs linked to the CPI or fixed minimum annual rent escalations. All in all, incremental cash rental revenue looks well poised to expand for the foreseeable future.

Then unlike quite a few of its peers, MPW does not suffer from any major concentration effect, which reduces the overall impact of potential bankruptcy risks tied to some of its operators (even when faced with bankruptcy challenges, MPW typically sets up master lease structures which enable it to reclaim all properties on default). Just to clarify, note that no single property accounts for more than 3% of its gross assets. MPW also does a very good job of extracting value from its assets. The average ROA of healthcare REITs only works out to 2.5%; MPW on the other hand generates ROAs that is more than 2x better than this figure at 5.7%!

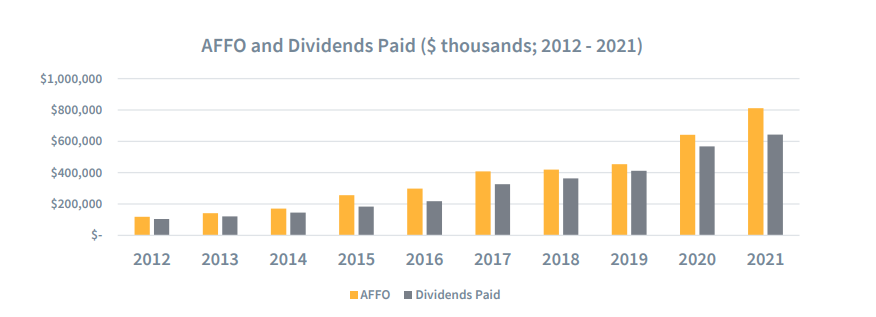

Then of course there’s the income angle to consider, something which appears to be very reliable and sound. MPW has been paying out quarterly dividends since 2005, and the dividends as a function of the company’s AFFO have typically come in at rather elevated levels of 80% (I will cover other aspects of the dividend towards the end of this article).

Company presentation- April 2022

Will Medical Properties Stock Go Up Again?

Technically, at current levels, the risk-reward on offer looks quite attractive, and it could attract some bargain-hunting ammunition that could serve as a useful fillip for the stock’s progress.

The first chart highlights the relative strength of the Medical Properties stock as against its peers in the Real Estate space, represented by the Vanguard Real Estate ETF (VNQ). We can see that over the years, MNQ has continued to gain more stature relative to VNQ in the shape of an ascending channel, and currently, that ratio is trading closer to the lower boundary of the channel, implying good risk-reward.

Stockcharts

Similarly, on the standalone monthly chart of MPW, we can see that the stock has been trending up in the shape of an ascending wedge, and after the correction witnessed since the start of the year, the stock recently bounced off the lower boundary of this wedge.

Investing

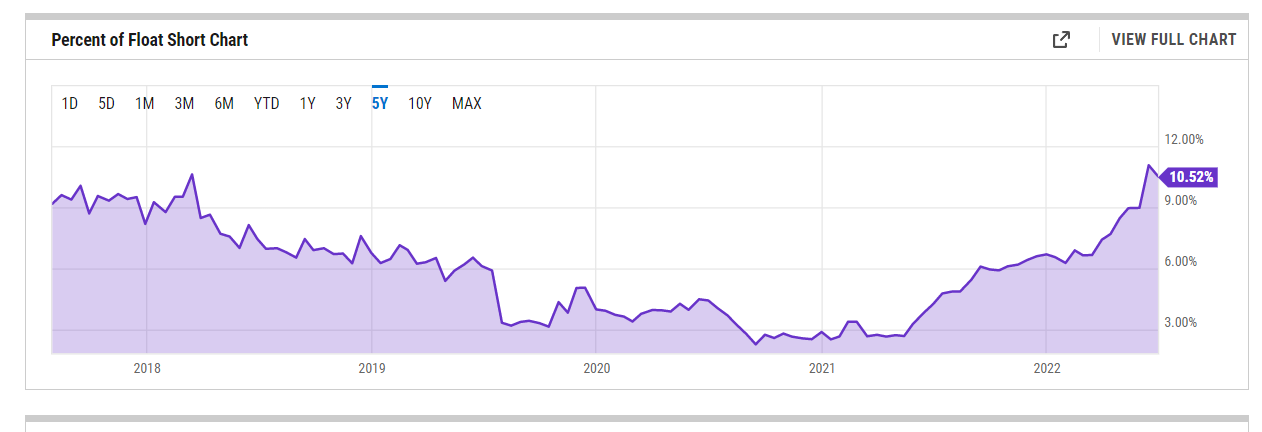

What could perhaps also abet potential upside momentum is the growing prospect of a short squeeze. Just to contextualize the situation, the number of shares that have been sold short but are yet to be covered has never quite been this high at nearly 45m shares. Put another way, that works out to almost 11% of the float that is currently short (typically, over the last 5 years, MPW’s float, that has been short, has averaged less than 6%) which could be closed out in the weeks and months ahead if an appropriate catalyst comes through.

YCharts

The most immediate catalyst on the anvil will be the Q2 results due to be announced on July 27. Consensus FFO estimates for Q2 (0.45) imply that it will be the weakest quarter before things pick up in Q3 and Q4. Do consider that as things stand, FY22 consensus is already at the upper end of the management’s previous FFO guidance of $1.78-$1.82 so any negative surprises in Q2 won’t be taken too well. Investors should be watching out for any updates with hospital labor costs as this appears to be putting a spanner in the works of hospital-related finances; in the Q1 call, the MPW management was keen to play down the impact of this, but recent data from Kaufman and Hall, show that even though hospital volumes remain resilient, labor market remains hyper-competitive resulting in negative operating margins.

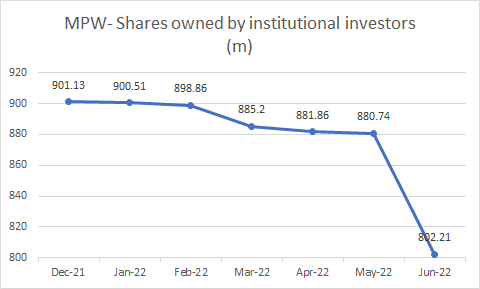

Having said all that, if one wants to see really strong momentum in this counter, I suspect one would need to see investors with deep pockets, aka the institutional investor community, come back on board; unfortunately, according to the latest available data, they have continued to reduce their ownership stake in MPW every month since the turn of the year (with June’s reduction being particularly pronounced).

YCharts

Closing Thoughts- Is MPW Stock A Buy, Sell, or Hold?

One of the principal reasons why some investors may have been reluctant to hold MPW is on account of a potentially slower pace of acquisitions, an important facet of the MPW story so far. Just for some context, last year, they spent around $3.9m on acquisitions, but this year, the acquisition forecast is expected to be much lower, within a range of $1-$3bn.

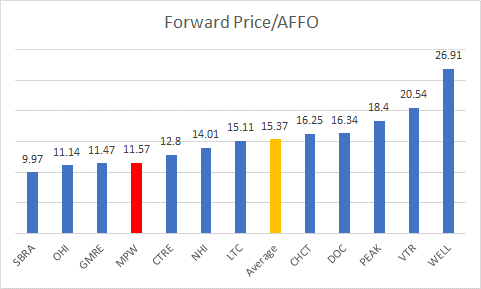

I can understand the reduced pace of acquisitions being a concern if the stock was still trading at pricey valuations, but that no longer appears to be the case. As you can see from the image below, on a forward price/AFFO basis (11.6x), MPW is one of the cheapest healthcare REITs around, trading at a 25% discount to the peer set average.

Seeking Alpha

Besides that, I would also point to the highly lucrative yield facet of MPW which could well be the raison d’être for most investors. At 6.9%, this is one of the highest yielders you could own from the health-care REIT space (the average yield on offer in this sector is considerably lower at only 5.34%). What also makes a potential ‘Buy’ timing right is the fact that at the current price point, MPW offers the most superior yield differential relative to its long-term average (of +130bps); no other healthcare REIT even comes close, with quite a few of them even offering yields lower than their long-term averages.

Seeking Alpha

All things considered, I would rate the MPW stock a BUY at this juncture.

from Top Stock To Invest – My Blog https://ift.tt/FMtg3w9

via IFTTT